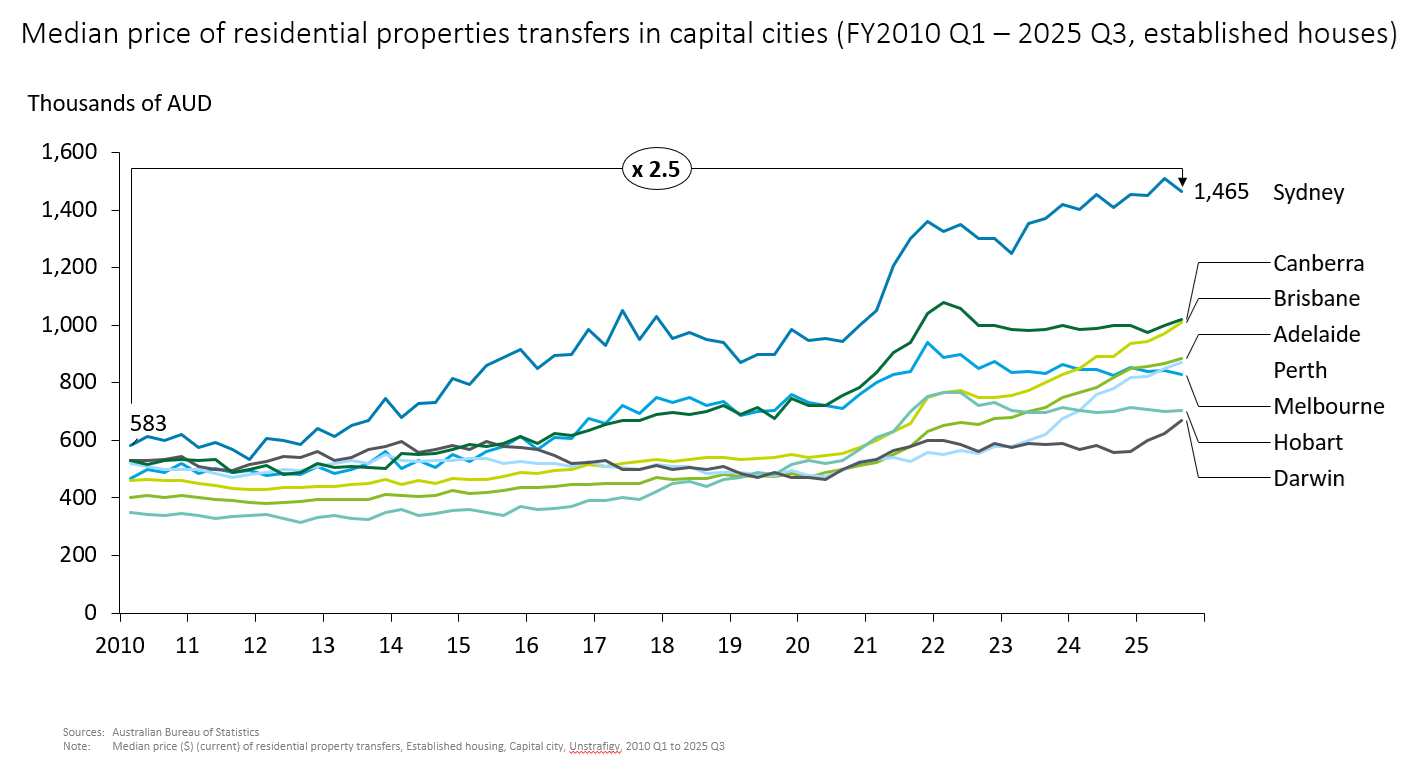

Figure 1

Australian housing prices are rising faster than Japan. In Sydney, for example, the median transaction price of a detached house jumped 2.5 times from about AUD580,000 in 2010 to about AUD1.46 million in the third quarter of 2025 (Figure 1). Why are Australian house prices rising so fast?

Behind the Rising Housing Prices – Demand Side

Since the rise in building costs is a global phenomenon, as is widely observed that the same thing is happening in Australia. So what is unique to Australia? First, we would like to explore the demand side.

The most significant factor is population growth. Although the birthrate in Australia is stagnant just like in other developed countries, it accepts more than 200,000 immigrants every year, and the population is increasing by around 400,000 annually. This will naturally increase the demand for housing, but the supply cannot keep up with this, which is increasing upward pressure on prices (The fact that they can cope with high prices is also significant because they are accepting mainly skilled workers with high wages.). [*2] In fact, it is reported that the housing vacancy rate is as high as 1.2% (as of September 2025), and considering that there are some properties with bad conditions that are not suitable for living in, there are virtually no vacancies. [*3] For this reason, once an application for rent is made, a large number of people who want to rent a house come to see it, and the application for occupancy becomes time-sensitive. In addition (although it is not obligatory), applicants are required to write a cover letter stating how suitable they are as a tenant.

The tax system is also a contributing factor. The system is designed to attract speculation. For example, an individual who is an Australian or a permanent resident holds assets for more than 12 months and is subject to tax only 50% of the gain on sale. Tax on gain through a sale of a property he/she has lived is even exempted. The government is considering tightening regulations on the practice of negative gearing, in which investors buy real estate for investment with loans, save taxes by accumulating profits and losses, and eventually sell the property to earn more than the investment losses. [*4] [*5]

Behind the Rising Housing Prices – Supply Side

Let's also look at the supply side. To address the housing shortage, the Albanese Government announced and launched the Homes for Australia plan in 2024, which aims to provide 1.2 million homes over 5 years by 2029 at a cost of AUD32 billion. [*6] However, delays were already pointed out in the following year, 2025, and it was reported that 180,000 units might fall short of the target in the final year. [*7] Why is it difficult to increase supply despite the government's efforts? There is no doubt that one of the reasons for the supply constraints is that higher material costs are making it harder for businesses to make profits. A closer look, however, reveals that there are many other factors involved.

First, infrastructure is insufficient. In order to develop housing, it is assumed that the infrastructure such as schools, medical institutions, roads, and public transportation, as well as electricity, gas, water and sewerage, has been developed. This has not caught up with Australia, whose population has grown rapidly from about 19 million in 2000 to about 27 million in 2024. In particular, the development of transportation systems requires enormous costs and an extremely long time. In this regard, although Japan suffered from a severe housing shortage after World War II, its transportation infrastructure, mainly railways, had been developed before World War II, so there were larger areas for housing development and it was possible to supply a large number of housing, including public housing.

Next, it takes a lot of time for government approvals for development and construction. As regulations, including those related to the environment, have increased and become more complex in recent years, the number of administrative agencies under their jurisdiction has also increased. Under such circumstances, it is said that due to insufficient information sharing, the time and effort required for applicants to obtain permits and licenses have increased significantly. In addition, it has become clear that the labor shortage, especially at municipal offices, has caused many inefficiencies, such as delays of about 6-12 weeks due to the inability to keep up with the process of granting addresses after construction is completed.

In addition, some local governments do not issue permits or licenses for large-scale housing development due to residents' concerns about the deterioration of the residential environment caused by rapid population growth and the deterioration of the landscape caused by high-rise buildings. The NIMBY ("Not In My Back Yard") trend is also strong, and it is a headwind to the supply of new housing. [*8] [*9]

Another major problem is that the construction industry's supply capacity is stagnant, and it is unable to undertake construction projects in quantity to meet demand.

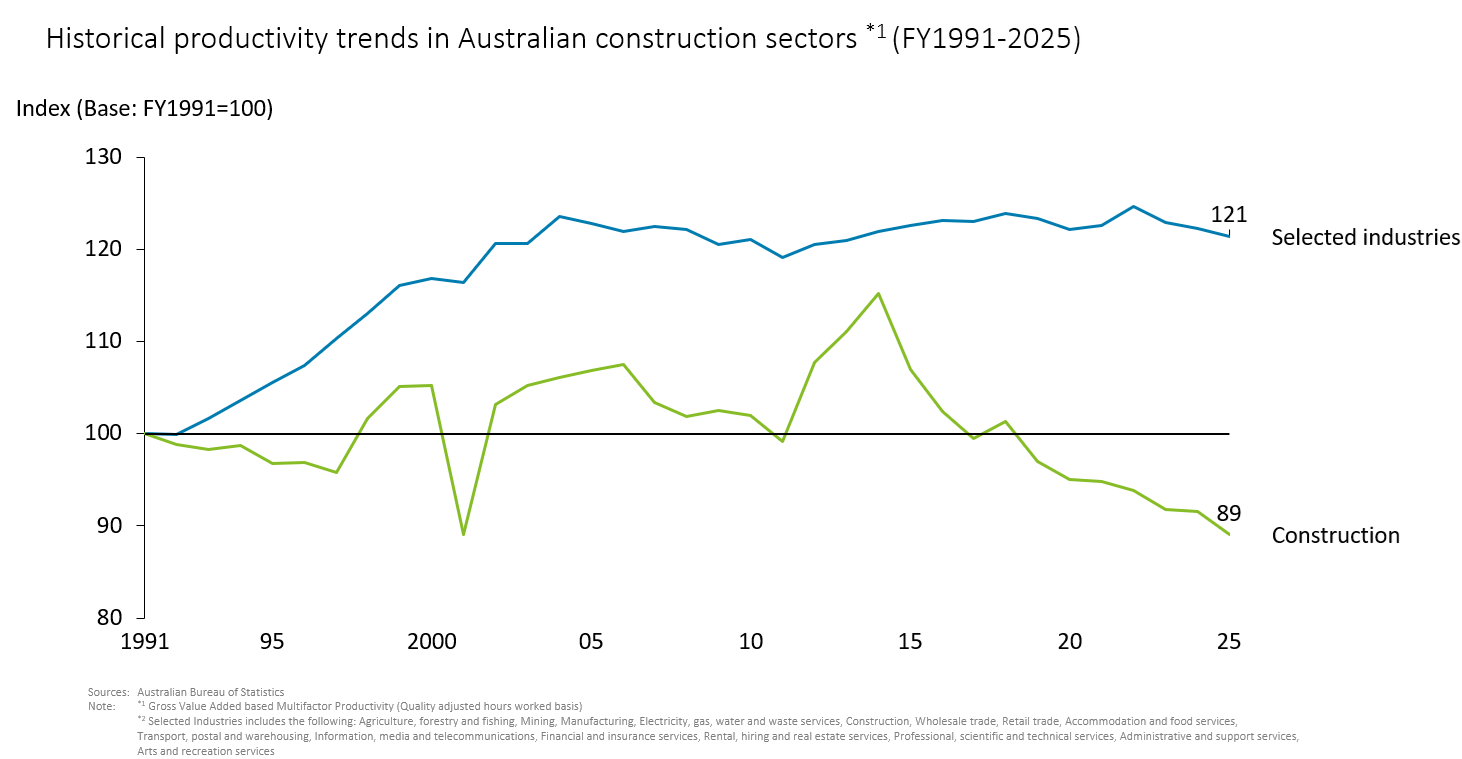

Sluggish Productivity in the Construction Industry

Figure 2

Low productivity in the construction industry has been pointed out as the cause of the sluggish growth in supply capacity in Australia. According to government statistics, when fiscal 1991 is set at 100, the productivity index for selected industries in fiscal 2025 increased to 121, while that for construction decreased to 89 (Figure 2). From the 1990s to the present, productivity has greatly improved across industries, driven by the spread of technologies including computers and the Internet. It is difficult to understand intuitively that productivity went down during this period. Why did this happen? The commonwealth government’s Productivity Commission's analysis identifies several structural factors as contributing factors. [*10]

First, the size of the company is small. In the construction industry, which has a subcontract structure, SMEs account for the majority of the industry, and the market share of the major 4 companies is only 12% (2012). This is in contrast to, for example, infrastructure and manufacturing, which account for around 60%. While the industry as a whole employs 5.5 people on average, construction companies employ only 2.7 people on average (1 person for home builders). At this size, it is extremely difficult to create economies of scale, such as increasing operational efficiency through the division of labor. The average number of workers employed by construction companies in Japan is 8.1, making Australia's size remarkably small. [*11]

Next, there is weak innovation. It has been pointed out that the Australian construction industry is more reluctant to utilize technology than other industries. As mentioned earlier, in recent decades, many industries have increased productivity by leveraging the evolution and spread of technology, including the computer Internet. The Australian construction industry, however, ranked last among 17 industries surveyed in terms of the use of data for the development of new products and services, and 14th (2017) in terms of the use of data for supply chain management. [*12] The reason for this, of course, is that they are too small to even think about using technology. Furthermore, it has also been pointed out that, since business is project-based, companies are repeatedly separated and reorganized for each project, making it difficult to accumulate and share knowledge and know-how that form the basis of innovation.

Furthermore, there are not enough craftsmen working on construction sites. As an immigrant country, Australia is likely to have an abundant supply of human resources. In particular, restrictions placed on immigration during the COVID-19 pandemic, until recently construction workers were not included as priority occupations for immigration, and the careful screening process for visas for construction workers took up to 18 months. As a result, the shortage of human resources has become significant and is still felt today. In addition, because profit margins are squeezed by rising construction costs and productivity is low, their ability to raise wages is limited, and they are unable to retain human resources and allow them to flow to other industries. There have been many government-led projects, including infrastructure construction, and it has been pointed out that the public and private sectors are competing for labor. [*13]

Impact of the Housing Shortage

As a result of a combination of factors, the balance between supply and demand has collapsed, leading to a rise in housing prices. And none of these factors can be resolved in the short term. Given the nature of real estate development, which takes several years at least from site acquisition to occupancy, this trend is likely to continue for some time.

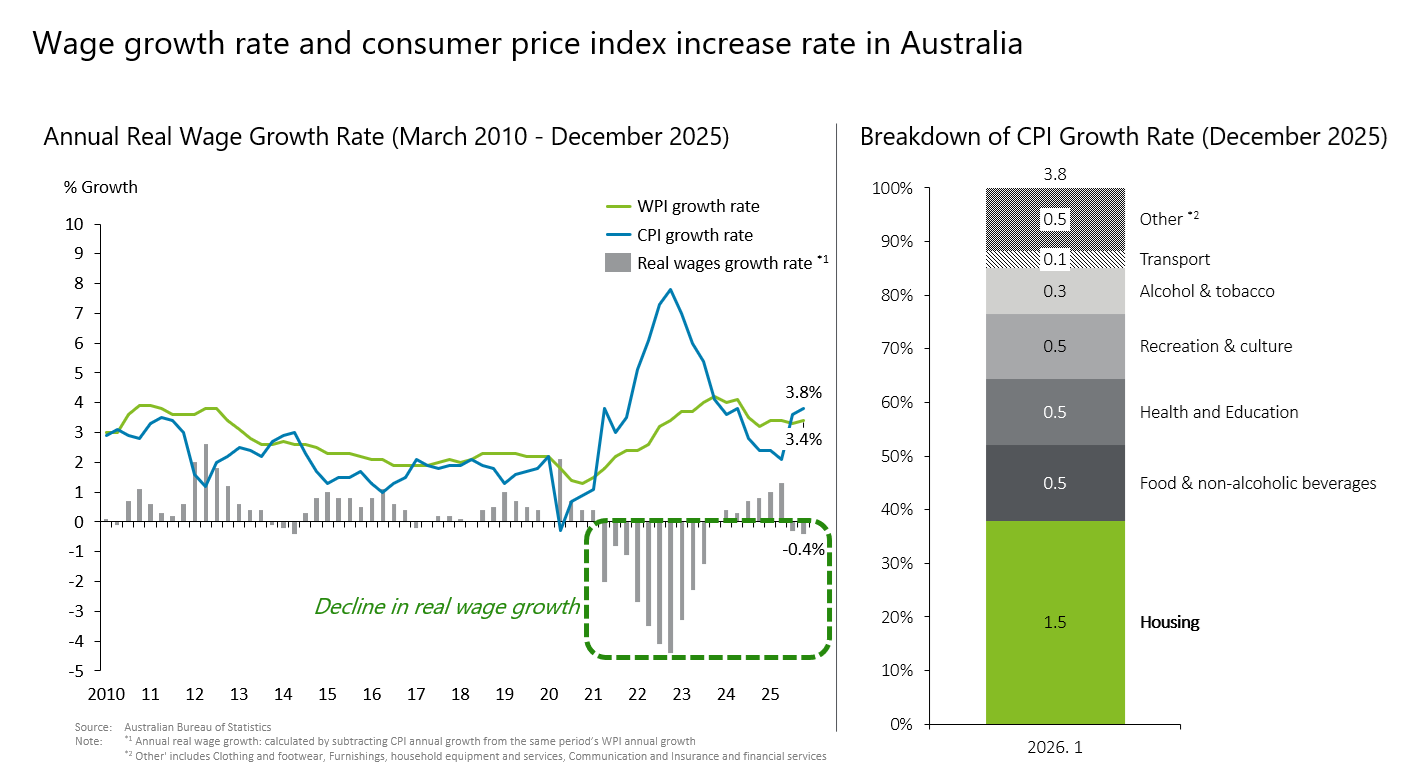

Figure 3

Complex and structural problems are causing a housing shortage, which is not easy to solve, but Australia cannot just wait and see. The Reserve Bank of Australia raised the cash rate in February 2026 for the first time in 2 years and 3 months (by 0.25% to 3.85%) in response to the acceleration in inflation (3.8% as of December 2025). Inflation is not expected to reach the 2 ~ 3% target band until the middle of 2027, suggesting further hikes. As wages have not kept pace with inflation, real wages have been on a downward trend, and this has become a source of concern for people. The biggest cause of this inflation is housing prices (Figure 3).

END

So far, we have focused on the mechanism of the housing shortage in Australia. Meanwhile, there is no doubt that it is an attractive market where demand far exceeds supply, growth is expected over the medium to long term, and geopolitical risks are low. As a result, Japanese real estate developers and house builders are expanding their businesses in Australia as they seek to diversify away from the domestic market, where medium- to long-term growth is uncertain. For example, major companies such as Mitsubishi Estate Co., Ltd., Mitsui Fudosan Co., Ltd., Hankyu Hanshin Fudosan Co., Ltd., Sumitomo Forestry Co., Ltd., and Asahi Kasei Homes Co., Ltd., have entered the market and established a solid position.

The partnership between Japan and Australia is deepening every year, not only politically but also economically, as developed countries in the Asia-Pacific region share common values. In 2025, Japanese investment in Australia reached a record high of JPY 13 trillion. [*14] The real estate sector is the driver of investment in Australia. In the real estate sector, the housing sector is a field where Japan, which has a solid track record and know-how but has a growing market, and Australia, which has a high market potential but faces a shortage of supply, can complement each other. Economic exchanges, including cooperation and M&A, between the two countries are expected to intensify in the future.

Under such circumstances, Japanese real estate developers and house manufacturers considering entering or expanding their business in Australia should consider preparing strategies and measures in advance to overcome supply constraints caused by multiple factors as mentioned in this article. Alliances with local companies and M&A are also options.

Deloitte Tohmatsu LLC and Deloitte Australia have a real estate team, an M&A advisory team, and members in charge of Japanese companies in both Japan and Australia, and have provided extensive support for collaboration and M&A in real estate and construction companies between the two countries, including business strategy studies, market research, and due diligence. If you are interested, please feel free to contact us.

[*1] the Ministry of Land, Infrastructure, Transport and Tourism

[*2] Australian Bureau of Statistics

[*3] SQM Research

[*4] NICHIGO PRESS

[*5] Commonwealth Bank

[*6] Australian Financial Review

[*7] Australian Financial Review

[*8] Australian Financial Review

[*9] Australian Financial Review

[*10] Productivity Commission

[*11] the Ministry of Health, Labour and Welfare

[*12] Productivity Commission

[*13] Casu Australia

[*14]Nikkei

Author

Kazuhiko Ota

Deloitte Tohmatsu LLC

Senior Manager

Kaz previously worked for a leading Japanese real estate developer, where he held senior overseas roles, including Deputy Head of the Taipei Office and Head of the Shanghai Office. He subsequently joined a global strategy consulting firm before joining Deloitte Tohmatsu Financial Advisory LLC (now Deloitte Tohmatsu LLC).

As a member of Deloitte’s Life Sciences, Healthcare & Sports Business Group, he has supported Japanese clients in the sports and healthcare sectors on a range of engagements, including M&A, market research, development of management plans, and evaluations of overseas market entry. He is currently based in Australia, where he supports Japanese companies in expanding into the Australian market.

Note: Company names, titles, and other details above are as of the publication date.