Industry size and trends

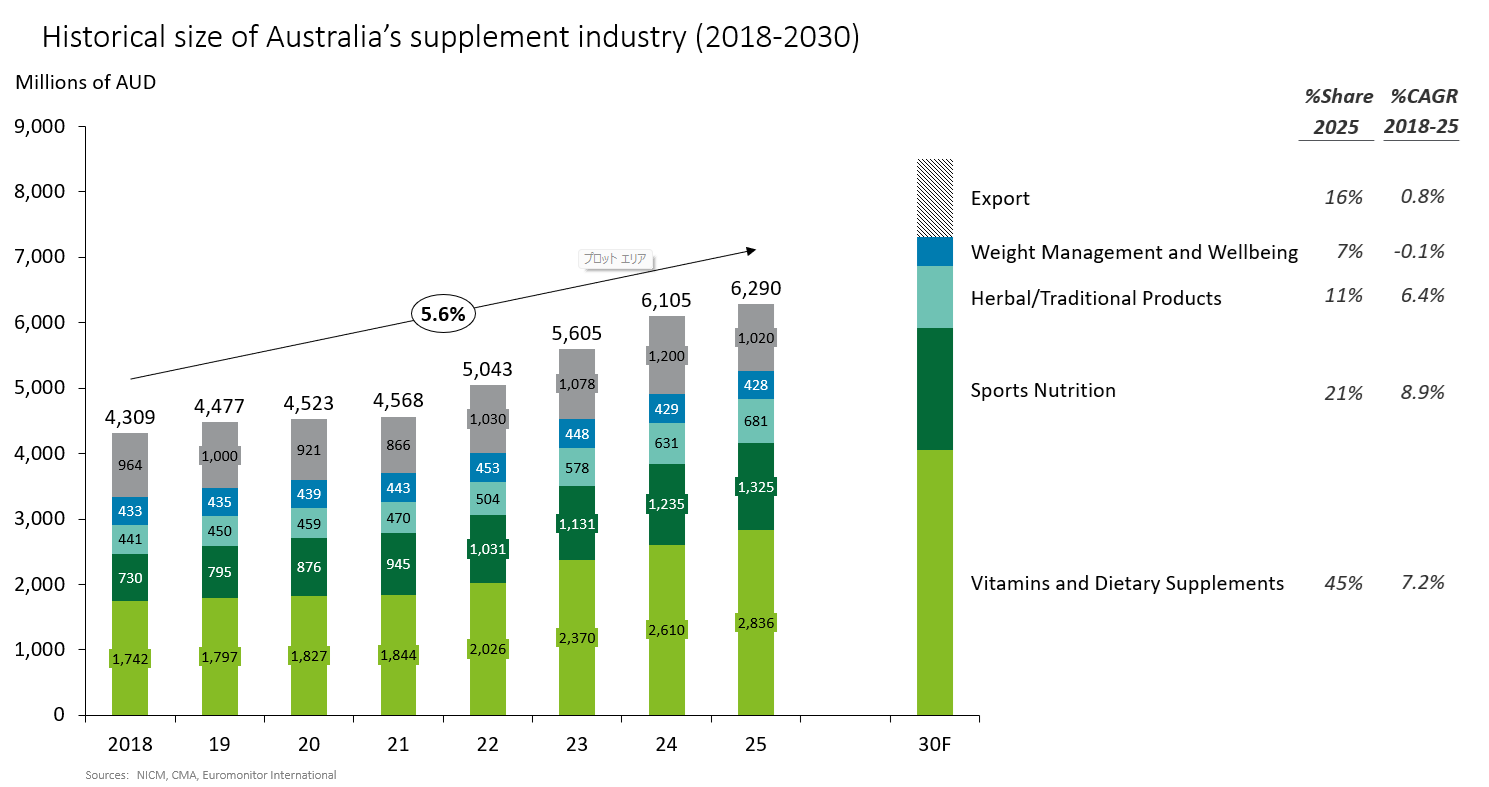

Let’s look at the overall picture of Australia’s supplement industry (Figure 1). As of 2025, the industry is estimated to be approximately AUD 6.29 billion (approximately JPY 629 billion assuming AUD 1 = JPY 100). Of this total, the vitamins and nutritional supplements segment accounts for 45%, sports-related products 21%, herbal and traditional products 11%, weight gain/obesity suppression products 7%, and exports a further 16%. From 2018 to 2025, the industry grew at a CAGR of 5.6%, and while export values can be a swing factor, continued growth is expected going forward[*2][*3].So what is driving this growth? A notable feature is that, beyond domestic market expansion, exports—which account for 16% of the total—have played a significant role. Exports grew from around AUD 0.96 billion in 2018 to AUD 1.2 billion in 2024 and are expected to continue increasing. Although this sits outside the range of the charted data, it is clear that from the mid 2010s Australian supplements rapidly gained popularity—particularly in East and Southeast Asia—leading to a sharp rise in export values. After easing temporarily during the COVID-19 period, exports have returned to an upward trend since 2022. In other words, the industry has successfully captured demand in fast growing emerging markets.

Popularity overseas

Why have Australian supplements been so strongly supported in emerging Asian markets? In general, products made in Australia—not only supplements but also foods and skincare—are widely perceived as high quality, safe, and “clean,” and this image is a major factor behind their popularity among foreign consumers, including Japanese. However, it is not easy to sustain such support over the long term on image alone. So what lies behind this enduring popularity? One decisive factor appears to be stringent manufacturing and sales regulations.

In other words, Australian supplements enjoy a reputation among domestic and overseas consumers for being high quality, safe, and “clean,” and this is supported not only by image but also by government involvement. Where regulation relies primarily on companies’ self-discipline, a quality incident like the “red yeast rice issue” can make it difficult to restore trust. By contrast, strict government regulation makes such incidents less likely and helps stabilize consumer trust. This is considered one important reason why Australian-made supplements have earned strong support not only at home but also across Asian markets.

Challenges

We have looked at the factors behind the popularity of Australian-made supplements, but the industry is not without challenges. Three major challenges are: (1) regulation, (2) supply chains and export destinations, and (3) productivity-related issues.

First, regarding regulation: as noted above, being regulated as complementary medicines rather than foods is one source of competitiveness for Australian supplements. On the other hand, it can also constrain business activity—for example, launching a new product containing a new ingredient can take more than one year to obtain regulatory approval (and in some cases up to around four years). Supplements are consumer products, and as seen in the steady stream of new offerings in stores—such as products for improved sleep quality or weight management—responding to consumer needs often requires bringing higher value added products with new ingredients to market in rapid cycles. As Australian brands seek to strengthen their presence overseas, excessive regulation could become a headwind and may even risk alienating domestic consumers. Strict regulation is a double edged sword. In this area, industry bodies such as Complementary Medicines Australia (CMA) and policy research institutions related to complementary medicines, such as the National Institute of Complementary Medicine (NICM), are advocating to the government for a regulatory approach that balances consumer access, safety, and industry growth[*6].

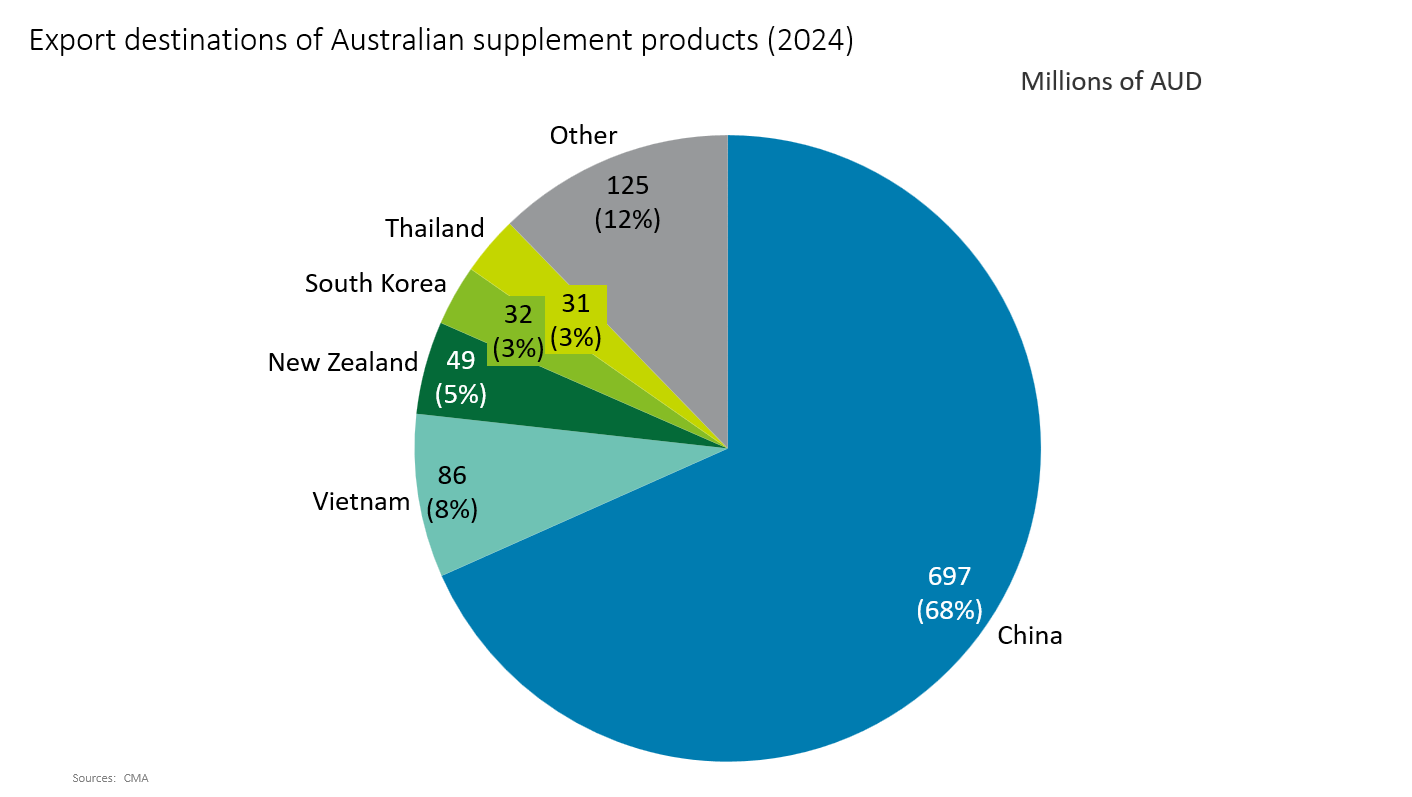

Next are supply chains and export destinations. While Australian supplements have a strong export presence, the reality is that as much as 99% of raw materials are imported (2021)[*7]. There is also a concentration of import sources—for example, 53.2% of vitamin raw materials are imported from China (2023)[*8]. As international conditions become more unstable, this high dependency could undermine the stability of the industry. Diversifying supply chains—by switching to domestically sourced raw materials and broadening import sources—will be important. Export destinations are also highly concentrated: China accounts for 68% of exports (2024)[*9]. Since 2020, China has repeatedly imposed sudden restrictions on Australian products—such as beef, barley, wine, lobster, coal, and iron ore—whenever bilateral tensions increased, and it would not be surprising if supplements became a target at some point. Australian supplements are also popular in Southeast Asia, but Vietnam—the second-largest destination after China—accounts for only 8% of export value, making risk hedging through export diversification indispensable.

Figure 2

Finally, there is productivity. Australia faces chronic labor shortages, and the impact is greater in industries that require highly skilled talent. Because the supplement industry operates under strict manufacturing and sales regulations, companies need to employ many professionals with advanced skills across R&D, manufacturing, and quality control, among others—making it one of the industries heavily affected. Some businesses reportedly find it difficult to increase output due to talent shortages. Hiring scarce skilled professionals also increases labor costs, putting pressure on profitability. Therefore, improving productivity is essential to increase output and revenue while securing sufficient profits.

Conclusion

In fact, when Blackmores—Australia’s largest supplement company and a well-known brand in Southeast and East Asia—became part of Kirin Holdings in 2023, CEO Symington expressed expectations that Blackmores’ growth strategy, including “strengthening the supply chain” and “(productivity-focused) operational simplification and cost reduction,” would be strengthened and accelerated through collaboration with Kirin[*10]. In addition, as part of synergy creation, initiatives are underway to increase value by combining Japan’s technological capabilities with Australia’s brand strength and sales channels—for example, attempting to launch Kirin’s plasma lactic acid bacteria products, already popular in Japan, into Asia-Pacific markets under the Blackmores brand (already launched in Taiwan in 2025).Deloitte Tohmatsu LLC, together with Deloitte Australia, provides broad support ranging from business strategy development and market research to collaboration and M&A between Japanese and Australian companies. Amid increasing instability in the international environment, Australia—sharing common values and offering socio-economic stability—has been attracting growing attention as an investment destination for Japanese companies. If you are interested, please feel free to contact us.

[*1] Share of population aged 65 and over (Japan vs Australia), 2024.

[*2] Market size estimate for Australia’s supplement industry (2025) and segment breakdown.

[*3] Australia supplement industry growth rate (CAGR) and outlook (2018–2025).

[*4] Consumer Affairs Agency (Japan) (2025): FY2024 review of the Foods with Function Claims system.

[*5] Reference on the classification of supplements as foods (Japan) and comparison with pharmaceuticals/medicines.

[*6] Complementary Medicines Australia (CMA) / National Institute of Complementary Medicine (NICM): proposals on balancing access, safety, and industry growth.

[*7] Estimate that ~99% of raw materials for Australian supplements are imported (2021).

[*8] Share of vitamin raw-material imports sourced from China (2023).

[*9] Export destination concentration: China share of Australian supplement exports (2024).

[*10] Source relating to Kirin Holdings’ acquisition of Blackmores (2023) and CEO Symington’s comments on strengthening the supply chain and productivity-focused operational simplification/cost reduction.

Author

Kazuhiko Ota

Deloitte Tohmatsu LLC

Senior Manager

Kaz previously worked for a leading Japanese real estate developer, where he held senior overseas roles, including Deputy Head of the Taipei Office and Head of the Shanghai Office. He subsequently joined a global strategy consulting firm before joining Deloitte Tohmatsu Financial Advisory LLC (now Deloitte Tohmatsu LLC).

As a member of Deloitte’s Life Sciences, Healthcare & Sports Business Group, he has supported Japanese clients in the sports and healthcare sectors on a range of engagements, including M&A, market research, development of management plans, and evaluations of overseas market entry. He is currently based in Australia, where he supports Japanese companies in expanding into the Australian market.

Note: Company names, titles, and other details above are as of the publication date.