Australia’s Healthcare System

So what does Australia’s healthcare system look like? Its most notable features are the GP system described above and, in principle, publicly funded care. Unlike Japan’s insurance-based model, Australia funds healthcare primarily through taxation under a scheme called Medicare, which covers Australian citizens and permanent residents.

Medicare is financed through general revenue and the Medicare levy. While the levy varies depending on income and family composition, it is generally set at 2% of taxable income.

That said, Medicare does not mean everything is covered. Unlike Japan’s “free access” system, in Australia public funding applies only when patients receive medical services specified under Medicare.

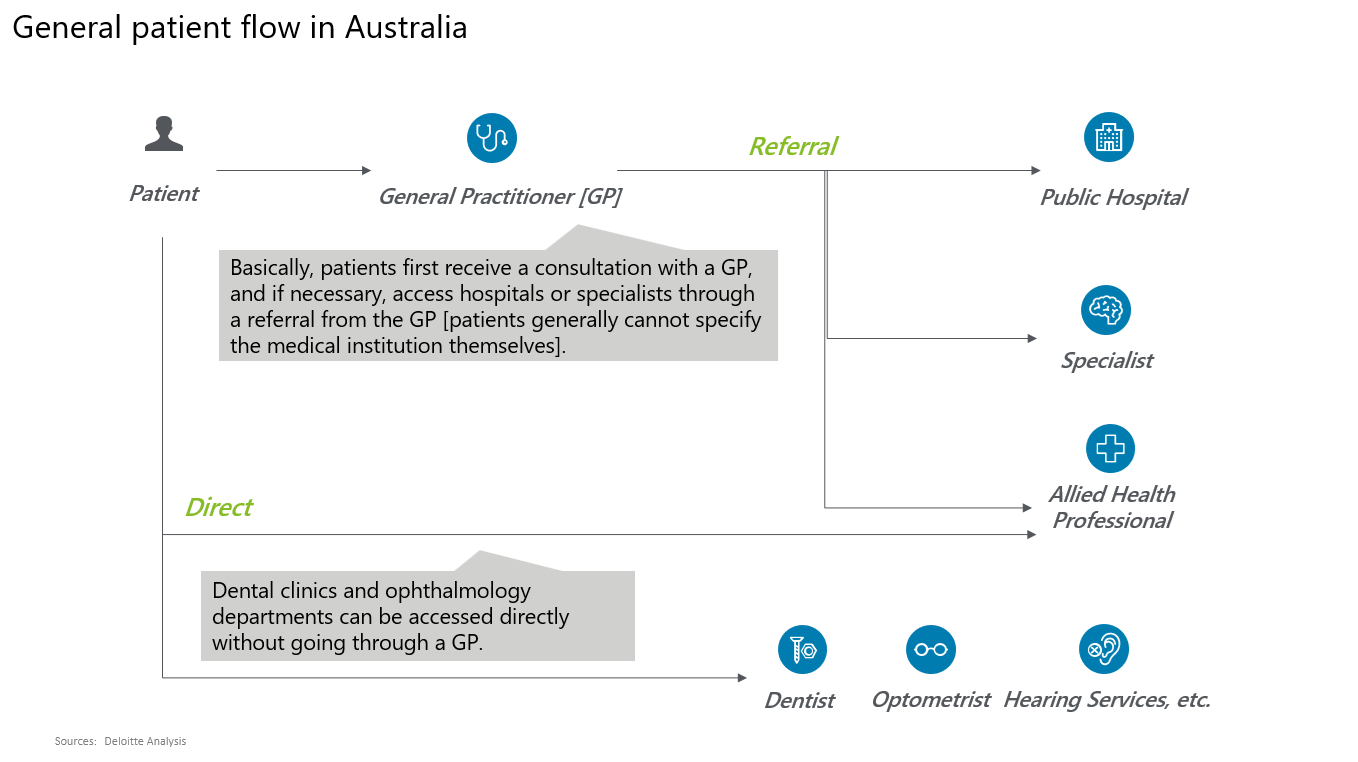

Figure 1

Across Australia’s vast territory, the number of public hospitals covered by Medicare is 701, with about 66,000 beds (2.5 beds per 1,000 people[*1] )—hardly reassuring capacity.

This is where GPs play a central role. In principle, patients are expected to see a GP first. Only when the GP determines that treatment by another provider is necessary does the patient receive a referral to a hospital, specialist, or other service (Figure 1).

As long as the service and fee fall within Medicare’s specified scope, the cost of GP visits and subsequent referred care is generally covered publicly, with no out-of-pocket payment. If a patient seeks services outside the GP’s judgement or outside Medicare’s specifications, the visit becomes self-funded.

By clearly defining the role of primary care and incorporating a physician’s clinical judgement into the patient pathway, the system aims to reduce unnecessary visits and allocate healthcare resources more efficiently.

Challenges of the GP System

That said, Australia’s healthcare system is far from problem-free. At first glance, it may appear to be an excellent mechanism that combines publicly funded services with managed patient pathways, but it is important to recognize that it is designed to optimize the system from the supply side.

From the patient’s perspective, the requirement to go through a GP—who is not a specialist—adds time and cost (and in some cases the GP’s services may fall outside Medicare’s scope, resulting in out-of-pocket charges). Moreover, within Medicare coverage there is very limited choice of provider, physician, or treatment. Patients who want greater autonomy are typically required to pay significantly more out of pocket.

Australia’s demographic and labor-market trends further compound these issues. Australia is widely known for continuing population growth driven largely by immigration, yet it is also ageing. People aged 65 and over accounted for roughly 16% of the population in 2020, and this is projected to rise to around 20% over the next 40 years[*2].

A key driver behind large-scale immigration is labor shortage. Shortages are particularly acute for highly skilled workers, and the government offers visas and permanent residency to individuals who meet certain conditions in occupations where shortages exist. Healthcare workers are among those occupations—meaning there is a shortage of healthcare professionals.

More broadly, Australia has long maintained relatively high wage levels compared with other advanced economies, consistently ranking among the OECD’s top 10 for average wages from the 1990s to the present [*3]. Since 2022, in the post-pandemic period, average wages have continued to rise at an annual rate of roughly 3%–4% [*4].

In this environment, healthcare workers—already in a highly competitive talent market—face particularly strong upward wage pressure. As a result, healthcare providers must absorb high personnel costs, raising the hurdle to securing sufficient staffing.

In short, while demand is rising due to population growth and ageing, supply is difficult to expand in line with demand because of workforce shortages and rising labor costs. In some regions it can be difficult to secure a GP appointment. Even after seeing a GP, patients referred onward may face significant delays because Medicare-covered public hospitals are operating at (or beyond) capacity, and long waits have become routine.

If a case is assessed as “not highly urgent,” it is not uncommon to be asked to wait several months—sometimes close to a year[*5] . There are also distressing cases in which a condition worsens during the waiting period (or a patient develops another illness), leaving them unable to receive treatment that might otherwise have been possible.

As in Japan, improving the productivity of healthcare providers is an urgent issue: the goal is to serve more patients without relying solely on headcount growth. This naturally heightens expectations for operating models and technologies that can mitigate workforce shortages.

Private Health Insurance

How do people respond? One approach is to purchase private health insurance. As noted above, services outside Medicare’s specifications require out-of-pocket payment, and private insurance can cover all or part of that patient-paid portion through benefits.

This enables patients to receive the services they want with greater peace of mind—without being overly constrained by long waits or large out-of-pocket costs (although, generally, out-of-pocket costs for GP visits are not covered by private health insurance). Options may include choosing particular treatments or selecting a private hospital rather than a public one.

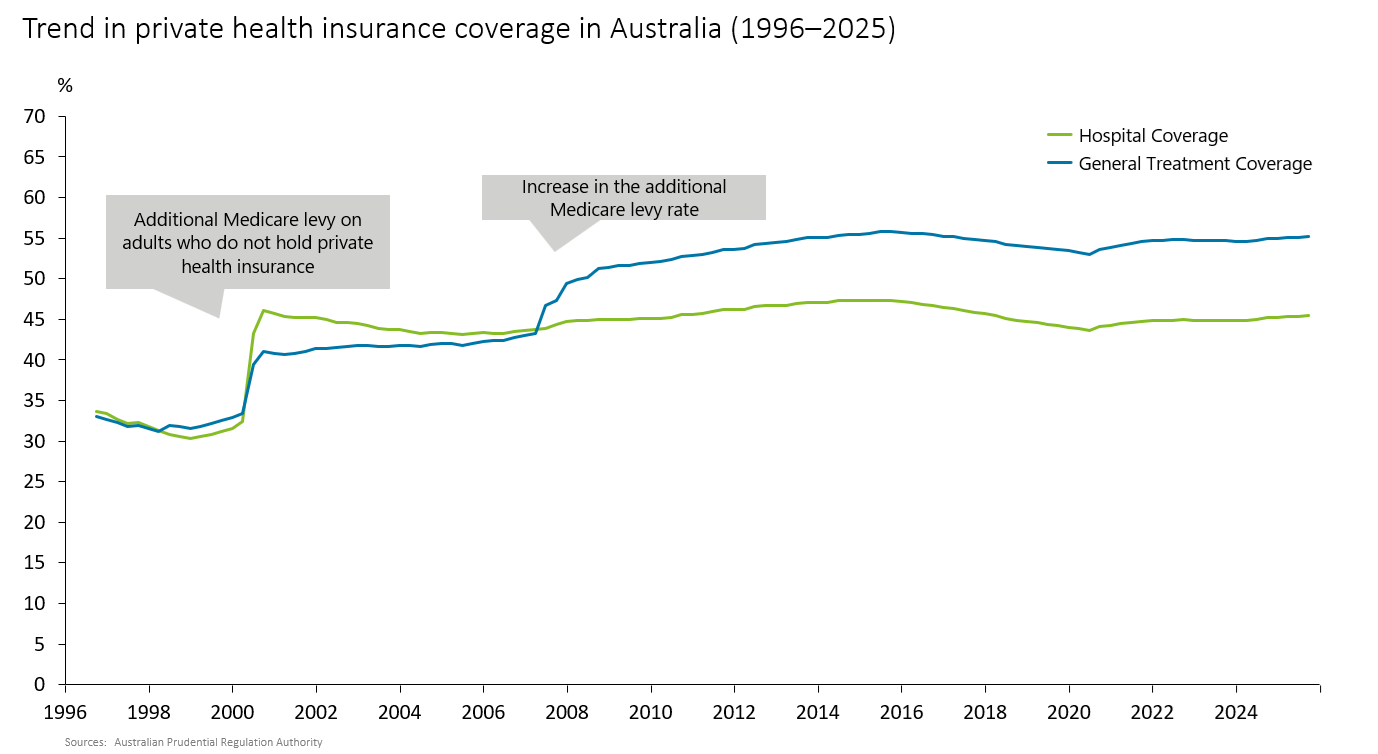

In fact, private health insurance participation has risen sharply: from roughly 30% in 2000 to, by 2024, about 45% holding Hospital Cover (covering hospital treatment costs) and about 55% holding General Treatment Cover (covering services outside hospitals). Because Medicare does not cover dental care or many optical expenses (e.g., glasses and contact lenses), demand is particularly strong for dental-related coverage.

The government also expects private health insurance to complement Medicare and has effectively encouraged enrollment—for example, by imposing an additional Medicare levy on certain higher-income individuals who do not hold private hospital cover (Figure 2).

Figure 2

Private health insurance, however, has its own challenges. Regulations require community-rated premiums within each region, and insurers are not permitted to price premiums based on individual risk or refuse applications[*6]. As a result, while the premium burden is broadly uniform, benefit payouts tend to be higher for older members with poorer average health—raising questions about intergenerational equity between contributions and benefits.

In addition, premiums have risen year after year due to medical advancement, inflation, higher labor costs, and population ageing. In 2025, for example, premiums increased by 3.73% year-on-year. In some years (such as 2015) increases exceeded 6%, often outpacing wage growth and inflation. This is a concern for Australians already facing declining real wages amid inflation.

Although it varies by plan and region, annual per-person private health insurance premiums in 2024 were reportedly around ¥3.2 million for younger people and around ¥4.2 million for middle-aged and older people (assuming 1 Australian dollar = ¥100), raising sustainability concerns[*7] .

Conclusion

Australia’s healthcare system and policy initiatives offer valuable lessons for Japan as it seeks ways to curb an ever-growing healthcare cost burden. While Australia’s system is highly rational from a supply-side perspective, it may not always be user-friendly from the demand-side perspective. As Japan moves toward a stronger family doctor system, it may face similar challenges and will need to address them.

At the same time, it is noteworthy that Australia has fostered a private health insurance market—still relatively limited in Japan. Given that the most pressing issue for healthcare providers is workforce shortage, there appear to be significant business opportunities for companies with operating models or technologies that improve productivity in clinical settings. For Japanese healthcare companies focused on productivity improvement, Australia may be a promising market for horizontal expansion.

Against a backdrop of growing demand, the relative visibility of upside from productivity gains, and resilience to economic cycles, private equity (PE) has also been actively investing in GP and dental chains. For example, in 2025 KKR invested in Family Doctor, a GP chain operating more than 100 clinics across Melbourne, Sydney, Brisbane, and other cities. Australian PE firm Crescent Capital invested in 2024 in the Australian subsidiary of Qualitas Health, which provides a range of healthcare services—including GP services—across Southeast Asia and Australia (Crescent has also expanded investments in dental and diagnostic imaging companies).

Deloitte Tohmatsu LLC, together with Deloitte Australia, provides broad support for business strategy development and market research, as well as partnerships and M&A between Japanese and Australian companies. Australia’s life sciences and healthcare sector remains in a phase of development and growth and is often described as a market with significant opportunities for Japanese firms. If you are interested, please feel free to contact us.

[*1] Australian Institute of Health and Welfare

[*2] Australian Institute of Health and Welfare

[*3] OECD

[*4] Australian Bureau of Statistics

[*5] Australian Institute of Health and Welfare

[*6] Department of Health and Aged Care

[*7] The Australian Financial Review

Author

Kazuhiko Ota

Deloitte Tohmatsu LLC

Senior Manager

Kaz previously worked for a leading Japanese real estate developer, where he held senior overseas roles, including Deputy Head of the Taipei Office and Head of the Shanghai Office. He subsequently joined a global strategy consulting firm before joining Deloitte Tohmatsu Financial Advisory LLC (now Deloitte Tohmatsu LLC).

As a member of Deloitte’s Life Sciences, Healthcare & Sports Business Group, he has supported Japanese clients in the sports and healthcare sectors on a range of engagements, including M&A, market research, development of management plans, and evaluations of overseas market entry. He is currently based in Australia, where he supports Japanese companies in expanding into the Australian market.

Note: Company names, titles, and other details are as of the publication date.